For years, the “glow-up” has been framed as a physical transformation—better skincare, a new wardrobe, hitting the gym, mastering makeup. But a quieter, more profound shift is taking place. Across generations, women are redefining what it means to truly level up. Financial independence is emerging as the ultimate glow-up—not because money buys happiness, but because economic power buys freedom, choices, and the ability to walk away from anything that no longer serves you.

This is not about rejecting beauty or self-care. It is about expanding the definition to include the kind of security that no face mask or outfit can provide.

Why Financial Independence Hits Different

The cultural script for women has long intertwined worth with appearance, caregiving, and partnership. Financial independence disrupts that script at its core. When a woman controls her own money, she controls:

Her Options: The ability to leave a job that undervalues her, a relationship that diminishes her, or a situation that endangers her.

Her Timeline: The freedom to make life decisions—marriage, children, career changes—on her own terms, not because she is financially dependent on another.

Her Voice: Economic power translates to bargaining power. In negotiations, in relationships, in life decisions, financial independence shifts the balance of who gets to set terms.

Her Future: The ability to invest in her own goals, support loved ones when needed, and build security that extends beyond her working years.

This is not materialism. It is liberation.

The Numbers Behind the Shift

The movement toward financial independence is visible in the data:

Women now control more than half of the personal wealth in the United States, a figure expected to grow as wealth transfers to younger generations

The number of women-owned businesses has grown at nearly double the rate of men-owned businesses over the past decade

Younger generations are prioritizing financial literacy and investment at higher rates than previous cohorts

Women are increasingly delaying marriage, having children later, and choosing partners based on partnership rather than provision

These trends reflect a fundamental reorientation: women are building their own tables, not waiting to be seated at someone else’s.

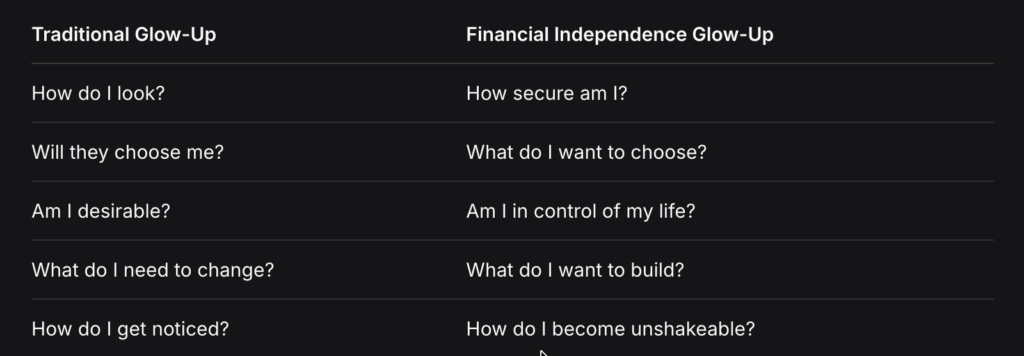

The Glow-Up Framework: From Appearance to Agency

The traditional glow-up focused on external validation—looking good enough to attract opportunities, partners, or approval. The financial independence glow-up is rooted in internal agency. It asks different questions:

This is not to say appearance is irrelevant. But financial independence reframes self-care as an investment in long-term stability, not short-term approval.

The Structural Reality: Why This Matters More for Women

Financial independence is not equally accessible to all, and it is not equally urgent for all. For women, the stakes are higher because:

The Gender Pay Gap: Women earn less over their lifetimes, meaning every dollar saved and invested carries disproportionate weight.

The Caregiving Penalty: Women are more likely to leave the workforce or reduce hours to care for children or aging parents, creating gaps in earnings and retirement savings.

Longer Lifespans: Women live longer than men on average, requiring more retirement savings while having earned less.

Higher Risk of Poverty in Old Age: Older women, particularly those who are unmarried or divorced, face significantly higher rates of poverty than older men.

The Marriage Risk: Financial dependence within marriage can trap women in unhappy or unsafe situations. Having independent resources is not about distrust—it is about ensuring that staying is a choice, not a necessity.

For women navigating these structural realities, financial independence is not aspirational self-help. It is a protective strategy.

How to Build Financial Independence: Practical Steps

The path to financial independence looks different for everyone, but foundational principles apply:

1. Get Clear on Your Numbers

Know your net worth (assets minus debts)

Track your spending for three months to understand where money actually goes

Understand your credit score and what affects it

2. Build a Safety Net

Aim for 3–6 months of living expenses in an accessible emergency fund

This fund is not for investments or splurges—it is for freedom when you need to walk away

3. Learn to Invest

Money sitting in savings loses value to inflation

Start with low-cost index funds; time in the market beats timing the market

Understand retirement accounts (401k, IRA) and maximize employer matches

4. Close the Knowledge Gap

Financial literacy is not taught in most schools; seek it out

Follow diverse financial educators (books, podcasts, courses)

Learn the basics of taxes, insurance, estate planning, and investing

5. Protect Your Earning Power

Negotiate salary and raises—women who negotiate increase lifetime earnings significantly

Invest in skills and education that increase earning potential

Consider side hustles, freelancing, or entrepreneurship if they align with goals

6. Build Your Village

Find trusted friends or communities to discuss money openly

Normalize conversations about salaries, investments, and financial goals

Work with fee-only financial advisors who have fiduciary duty to act in your interest

7. Plan for Interruptions

Factor in potential caregiving years

Consider disability and life insurance to protect against unexpected events

Build flexibility into your financial plan

The Emotional Shift: More Than Numbers

True financial independence is not just about reaching a specific dollar amount. It is about shifting your relationship with money from scarcity to agency. This involves:

Letting go of guilt: Spending on yourself is not selfish; it is sustainability. Saving is not deprivation; it is future freedom.

Rejecting the “princess” narrative: Waiting to be taken care of is not a life plan. Partnership is about mutual support, not dependency.

Building confidence: Financial literacy builds competence. Competence builds confidence. Confidence changes how you move through the world.

Redefining success: Success is not just what you earn, but what your money enables you to do, say, and become.

The Ripple Effect

When women achieve financial independence, the effects radiate outward. Daughters grow up seeing women in control of their own futures. Partners learn what true partnership looks like. Communities gain economic stability. Industries shift when women have the capital to invest in what they value.

This is not about rejecting love, partnership, or community. It is about ensuring that those relationships are chosen, not required. It is about showing up as a whole person, not a dependent.

The Bottom Line

The glow-up that matters most is not visible in a mirror. It shows up in bank statements, in investment accounts, in the ability to say “no” without fear and “yes” without hesitation. It is the quiet confidence of knowing that your life is yours to build, not someone else’s to provide.

Financial independence does not solve everything. It does not guarantee happiness or protect from loss. But it does something essential: it gives you the foundation to weather what comes, choose what matters, and design a life that is authentically yours.

That is the glow-up worth pursuing.

FAQ:

Q: Does financial independence mean I should never rely on a partner?

A: No. Financial independence is about having options, not about rejecting interdependence. Healthy relationships often involve shared resources and mutual support. The goal is that staying in a relationship is a choice, not a necessity due to lack of options.

Q: I earn less than my partner. Can I still be financially independent?

A: Financial independence is about having your own resources and agency, not about matching your partner’s income. Even with lower earnings, you can maintain separate savings, retirement accounts, and the ability to make independent decisions. The key is ensuring your financial life is not entirely controlled by another person.

Q: How much money do I need to be “independent”?

A: There is no universal number. Financial independence is the ability to cover your essential expenses and make choices without being forced by financial constraints. For some, this means a robust emergency fund and career skills. For others, it means investment income covering basic needs. Define it for your life and circumstances.

Q: I’m starting late. Is it too late to build financial independence?

A: No. The best time to start was ten years ago. The second-best time is today. Every step—even small ones—builds momentum. Focus on what you can control now: increasing savings rate, reducing debt, learning to invest, and protecting your earning power.

Q: What if I have debt? Can I still work toward independence?A: Yes. Managing debt is part of building financial independence. Prioritize high-interest debt while maintaining an emergency fund. A structured plan to reduce debt while building savings is a form of progress, not failure.